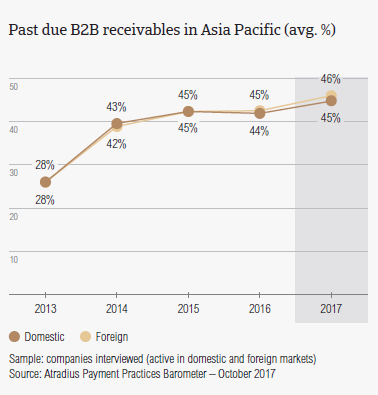

After a minor decrease from 45.0% in 2015 to 44.3% in 2016, the percentage of overdue B2B invoices in Asia Pacific increased again this year to 45.4%.

Emerging Asia remains the fastest growing economic region in the world with expected growth rates of 5.8% in 2017 and 5.6% in 2018. However, China’s economic growth will slow down in the medium term and several economies in the Asia Pacific region are sensitive to this development. A high percentage of respondents in the region stated their intention to increase credit management practices to better protect their businesses against the potential impact of slower growth.

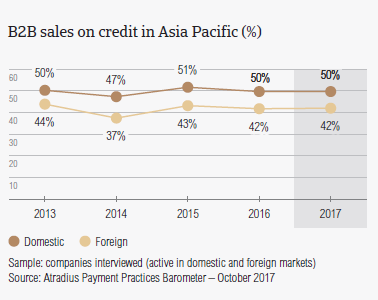

Sales on credit terms

With an average of 45.9% of B2B sales on credit terms, there hasn’t been a meaningful change in the propensity of respondents in Asia Pacific to use this method of payment compared to 2016 (46.2%). Credit sales continue to account for a higher proportion of B2B sales than that seen in Europe (40.0%) and in the Americas (45.5%).

- As shown in previous surveys, respondents in Asia Pacific are more likely to sell on credit to domestic B2B customers (49.5%) than to foreign B2B customers (42.2%). This seems to be a common preference among respondents in the Asia Pacific countries surveyed.

- Respondents in Japan (53.7%) seem to be the most inclined to offer credit terms to their domestic and foreign B2B customers. The country has also seen an increase compared to 2016 (52.0%), when credit sales were already more commonly than cash terms.

- In contrast, and despite an increase observed in 2017, respondents in China (40.7%) have shown the least credit friendly stance of the Asia Pacific countries surveyed.

Overdue B2B invoices (%)

After a minor decrease from 45.0% in 2015 to 44.3% in 2016, the percentage of overdue B2B invoices in Asia Pacific increased again this year to 45.4%.

- 89.6% of respondents in Asia Pacific reported late payments from their domestic B2B customers. This percentage increased slightly from the 88.3% registered in 2016. On average, 44.6% of their domestic invoices, remained unpaid at the due date.

- 88.8% of respondents reported that they experienced late payments from foreign B2B customers, the same percentage as in 2016. However, the proportion of foreign invoices that remained unpaid at the due date increased slightly from 44.6% in 2016 to 46.1% in 2017.

- The average frequency of late payments was the highest in China (domestic 93.9%, foreign 96.0%) and the lowest in Japan (domestic 67.3%, foreign 74.7%).

- Similarly to what was observed one year ago, India seems to be the country most impacted by late payment of invoices: 56.4% of the total value of domestic and 50.3% of the total value of foreign invoices were paid late. This is also reflected in the country’s DSO figure, which averaged 49 days and is higher than the regional average of 40 days.

- The percentage of overdue B2B invoices in Asia Pacific (45.4%) is lower than that registered in the Americas (48.8%) but slightly higher than that in Europe (41.1%).

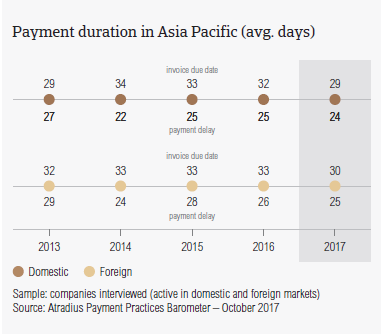

Payment duration (average days)

The average payment duration for Asia Pacific decreased from 59 days in 2016 to 55 days this year. This follows a shortening of payment terms and fewer payment delays than in 2016.

- In 2017, payment terms granted by respondents in Asia Pacific averaged 30 days (2016: 33 days).

- Average payment terms in Japan (44 days), Taiwan (43 days) and Hong Kong (31 days) are longer than the regional average.

- Similarly to what was observed one year ago, Japan offered the most lenient payment terms in the region. The average payment term given to domestic B2B customers was 45 days (45 days in 2016), while foreign B2B customers needed to settle their invoices, on average, within 42 days (43 days in 2016).

- With the exception of Australia and Taiwan, all countries surveyed in the Asia Pacific region saw a decrease in domestic payment delays. Respondents in Indonesia reported no changes in domestic payment delays.

- In respect to their foreign B2B customers, respondents in Taiwan and Indonesia reported an increase in payment delays in 2017.

- Respondents in Australia have the shortest average invoice to cash turnaround (around 44 days), and respondents in Taiwan the longest (71 days).

Key payment delay factors

Despite a decrease in the percentage of respondents citing insufficient availability of funds in 2017 (38.6% vs. 40.2% in 2016), this remains the most often cited reason for payment delays in the Asia Pacific region.

- Respondents in the Asia Pacific countries surveyed reported that their domestic buyers delayed payments most often due to insufficient availability of funds (43.8%), and the complexity of the payment procedure (27.4%).

- Insufficient availability of funds: 33.3%, and complexity of the payment procedure: 34.9% were also the primary payment delay factors of the foreign B2B customers of respondents in Asia Pacific.

- In addition to the Asia Pacific region, insufficient availability of funds was the main reason for domestic and foreign payment delays in the Americas (domestic: 41.8%; foreign: 28.3%) and Europe (domestic: 55.5%; foreign: 34.1%).

- India (51.5%) and Indonesia (50.5%) are the countries most impacted by late payments due to domestic customers’ insufficient funds. Foreign payment delays driven by the same reason were reported to occur most often in Hong Kong (38.4%), Indonesia and China (both with 34.9%).

Protection of business profitability

30.3% of respondents in Asia Pacific plan to do more to protect their businesses from the impact of Brexit, the slowdown in Asia and US protectionism. This is a significantly higher percentage than those registered in the Americas (25.9%) and in Europe (15.5%) and may highlight the respondents’ perception that they are more exposed to risk than their peers in other regions surveyed.

- 39.8% of respondents in Asia Pacific said that they do not intend to make changes in their current mix of credit management tools. This is the lowest percentage of the regions surveyed (the Americas: 41.7%; Europe: 50.8%).

- The two credit management tools preferred by respondents in Asia Pacific are checks on buyers’ creditworthiness (reported by an average of 36.1%) and monitoring buyers’ credit risk (34.0%). These were also the two most preferred credit management tools in the Americas and Europe.

- Although most worried about the slowdown in Asia, respondents in Asia Pacific seem to opt for the same management tools to protect themselves against potential risks stemming from all three developments. More specifically: Brexit (increasing creditworthiness checks: 31.2%; increasing credit risk monitoring: 31.9%), US protectionism (increasing creditworthiness checks: 35.6%; increasing credit risk monitoring: 33.4%) and the slowdown in Asia (increasing creditworthiness checks: 41.4%; increasing credit risk monitoring: 36.7%).

Find out more about how Atradius can support your credit insurance requirements.

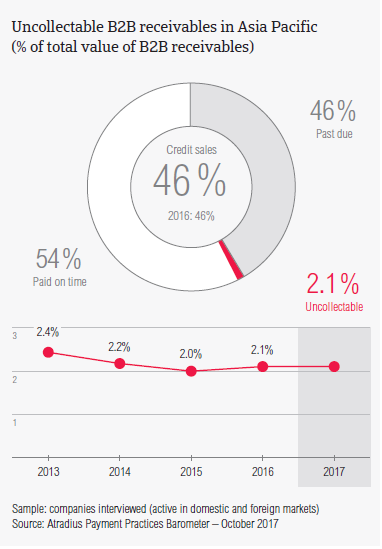

Uncollectable receivables

The proportion of B2B receivables reported by respondents in Asia Pacific as uncollectable is 2.1%, the same level as that registered in 2016. Moreover, it is higher than the proportion of uncollectable receivables reported in Europe in 2017 (1.2%) and matching that reported in the Americas (2.1%).

- Domestic receivables were written off as uncollectable more often than foreign receivables (domestic: 1.5%; foreign: 0.6%).

- With the exception of Australia (1.6%), in 2017 all countries surveyed in the Asia Pacific region reported an average percentage of uncollectable receivables around or slightly above the 2.1% regional average.

- Similarly to what was observed in 2016, India reported the highest proportion of uncollectable receivables (domestic: 1.8%; foreign: 0.8%).

- Uncollectable domestic receivables in Asia Pacific originated most often from the consumer durables, construction, electronics and business services sectors.

- B2B receivables were reported to be uncollectable mainly because the customer went bankrupt or out of business (47.4%), the old age of the debt (36.2%) and the inability to locate the customer (35.4%).

Payment practices by industry

Looking ahead, more respondents in Asia Pacific expect a slight deterioration than an improvement in the payment behaviour of their B2B customers over the coming 12 months.

- Respondents in the countries surveyed in Asia Pacific extended the most lenient payment terms to B2B customers in the metals and paper (40 days from the invoice date), machines (35 days) and chemicals (34 days) sectors. The shortest payment terms were granted to B2B customers in the consumer durables (27 days) and financial services (28 days) sectors.

- Customers in the construction and consumer durables sectors generated some of the longest delays. B2B customers in these sectors, paid on average 31 days and 33 days late respectively.

- The most frequently cited reason for late payment of invoices was insufficient availability of funds, reported by 43.0% of respondents in the construction sector and by 51.0% of respondents in consumer durables.

- 32.0% of respondents in the construction industry cited the complexity of the payment procedure as one of the main reasons for payment delay. Customers in the consumer durables sector cited the formal insolvency of the buyer and that the goods delivered or services provided did not correspond to what was agreed in the contract (36.0% for each of the two reasons) as reasons for payment delay.