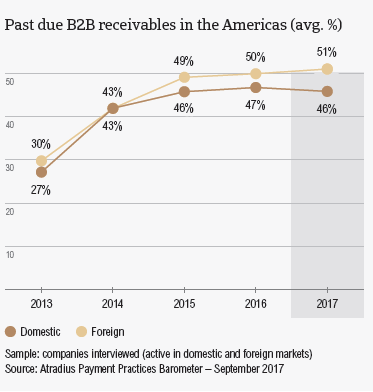

After a minor increase from 47.6% in 2015 to 48.4% in 2016, the percentage of overdue B2B invoices appears to be flattening out, rising to 48.8% in 2017.

The vulnerabilities brought by the new Trump administration together with the renegotiation of NAFTA and other political challenges, may be reasons why in 2017 respondents in the Americas plan to do more to protect their businesses from risks arising from US protectionism.

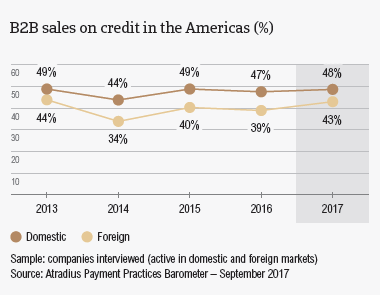

Sales on credit terms

With 45.5% of B2B sales on credit terms, respondents in the Americas seem slightly more inclined to use this method of payment than in 2016 (43.0%). The increase in the proportion of total B2B sales on credit in the Americas shows a contrasting trend to what was observed in Europe, where B2B sales on credit terms declined slightly from 41.0% in 2016 to 40.0% in 2017.

- As shown in previous surveys, respondents in the Americas are more likely to sell on credit to domestic B2B customers (48.3%) than to foreign B2B customers (42.6%).

- With the exception of the United States which showed no clear preference (domestic: 46.2%; foreign: 44.7%), all other countries surveyed in the Americas (Canada, Mexico, Brazil) seem to be more averse to offering credit terms to foreign B2B customers than to domestic B2B customers.

- Compared to 2016, all countries surveyed in the region increased their B2B sales on credit terms. Brazil and Canada have shown the most credit friendly stance (with 47.7% and 45.9% sold on credit).

Overdue B2B invoices (%)

Following a minor increase from 47.6% in 2015 to 48.4% in 2016, the percentage of overdue B2B invoices in the Americas appears to be flattening out, rising to just 48.8% in 2017.

- 92.6% of respondents in the Americas (2016: 95.0%) reported late payments from their domestic B2B customers. An average of 46.2% of the proportion of domestic invoices, remained unpaid at the due date.

- The frequency of late payments from foreign B2B customers decreased slightly from 91.0% in 2016 to 90.0% this year. In contrast, the proportion of foreign invoices that remained unpaid at the due date increased slightly from 50% in 2016 to 51.4% this year.

- The average frequency of late payments to respondents was highest in the United States (domestic 96.2%, foreign 94.0%) and lowest in Canada (domestic 88.7%, foreign 86.1%).

- Similarly to what was observed in previous surveys, Mexico seems to be the country most impacted by late payments of invoices; 54.8% of the total value of domestic and 56.0% of the total value of foreign invoices were paid late. This is also reflected in the country’s DSO figure, which averaged 47 days and is significantly higher than the regional average of 35 days.

- The percentage of overdue B2B invoices is higher in the Americas (48.8%) than in Europe (41.1%).

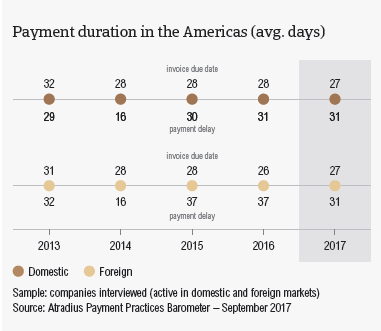

Payment duration (average days)

At regional level, the average payment duration is 61 days in 2017. This follows a shortening of the average payment terms and a modest decrease in payment delays in most of the countries surveyed.

- In 2017, payment terms granted by respondents in the Americas averaged 27 days (2016: 27 days).

- Average payment terms in Mexico (36 days) and Brazil (32 days) are longer than the regional average.

- Mexico offered the most lenient payment terms in the region. The average payment term given to domestic B2B customers was 35 days (33 days in 2016), while foreign B2B customers needed to settle their invoices, on average, within 36 days (32 days in 2016).

- With the exception of Mexico, all countries surveyed in the Americas saw a decrease in domestic payment delays.

- In respect to their foreign B2B customers, all respondents in the Americas (with the exception of Brazil) reported an increase in payment delays in 2017.

- Based on the above-mentioned changes, respondents in Canada have the shortest average invoice to cash turnaround (around 53 days), and respondents in Mexico the longest (75 days).

Key payment delay factors

The most often cited reason for payment delays among B2B customers of respondents in the Americas remains insufficient availability of funds.

- Domestic B2B customers of respondents surveyed in the Americas delayed payments most often due to insufficient availability of funds (41.8%), and their buyers’ intentional use of outstanding invoices as a form of financing (28.2%). While the main reasons for domestic payment delays were consistent with those of Europe (insufficient availability of funds: 55.5%; buyers’ intentional use of outstanding invoices as a form of financing 30.3%), the response rate for insufficient availability of funds was much higher in the Americas.

- Foreign B2B customers of respondents in the Americas most often delayed payments because of the complexity of the payment procedure (cited by 29.7%) and insufficient availability of funds (28.3%). The main reason for foreign payment delays in Europe was insufficient availability of funds (34.1%), followed by the complexity of the payment procedure (28.2%).

- Canada (48.6%) and Mexico (40.8%) are the countries most impacted by late payments due to domestic customers’ insufficient funds. Foreign payment delays driven by liquidity issues were reported most often in the United States (29.7%) and Canada (28.7%).

Protection of business profitability

25.9% of respondents in the Americas plan to do more to protect their businesses from the impact of Brexit, the slowdown in Asia and US protectionism. This is a significantly higher percentage than that registered in Europe (15.5%) and may highlight the respondents’ perception that they are more exposed to the risks arising from these developments.

- Similarly to what was observed in other regions surveyed, the majority of respondents in the Americas (41.7%) reported that they will make no changes in their current mix of credit management tools.

- On average, 31.9% of respondents in the Americas reported their intention to increase checks on buyers’ creditworthiness and 28.2% to increase monitoring of buyers’ credit risk in the face of the above-mentioned developments. These were also the two credit management tools most reported in Europe, although the percentages were significantly lower (20.0% and 17.4% respectively).

- Although most worried about US protectionism, respondents in the Americas seem to opt for the same management tools to protect themselves against Brexit (increasing creditworthiness checks: 29.6%; increasing credit risk monitoring: 26.2%), the slowdown in Asia (increasing creditworthiness checks: 30.9%; increasing credit risk monitoring: 27.6%) and US protectionism (increasing creditworthiness checks: 35.3%; increasing credit risk monitoring: 30.8%).

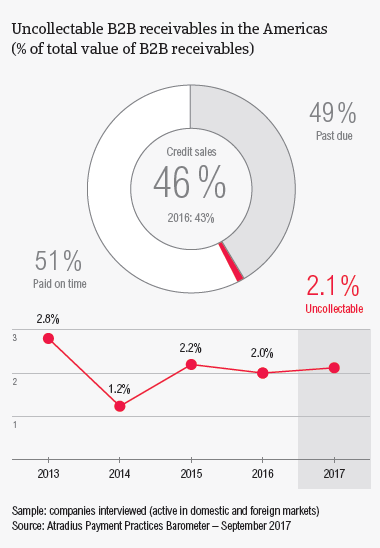

Uncollectable receivables

The proportion of B2B receivables reported by respondents in the Americas as uncollectable is 2.1%, slightly higher than the level reported in 2016 (2.0%). Moreover, it is higher than the proportion of uncollectable receivables reported in Europe in 2017 (1.2%).

- Domestic receivables were written off as uncollectable more often than foreign ones (domestic: 1.5%; foreign: 0.6%).

- With the exception of Canada, all countries surveyed in the Americas region reported an average percentage of uncollectable receivables around or slightly above the 2.1% regional average.

- Similarly to what was observed in 2016, Brazil reported the highest proportion of uncollectable receivables (domestic: 1.8%; foreign: 0.7%).

- Uncollectable domestic receivables in the Americas originated most often from the construction, consumer durables, electronics and business services sectors.

- B2B receivables were reported to be uncollectable mainly because the customer went bankrupt or out of business (50.6%), the old age of the debt (35.2%) and the failure of collection attempts (34.4%).

Payment practices by industry

Looking ahead, more respondents in the Americas expect a small improvement than a deterioration in the payment behaviour of their B2B customers over the coming 12 months.

- Respondents in the countries surveyed in the Americas extended the most lenient payment terms to B2B customers in the machines (37 days from the invoice date), textiles (33 days) and the transport (30 days) sectors. The shortest payment terms were granted to B2B customers in the construction and financial services (19 days each) sectors.

- Customers in the construction and construction materials sectors generated some of the longest delays. B2B customers in these sectors, paid on average 27 and 39 days late respectively.

- The most frequently cited reason for late payment of invoices was insufficient availability of funds, reported by 43.0% of respondents in the construction sector and by 44.0% of respondents in construction materials.

- 32.0% of respondents in the construction industry cited the complexity of the payment procedure as a main reason for payment delay. The second most cited reason by 35.0% of customers in construction materials was disputes over the quality of goods and services provided.